Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

March 2023 Real Estate Market Update

A recent surge in purchase activity indicates that the early spring real estate market is in full swing in our region. Fluctuating interest rates have caused some buyers to converge on properly-priced listings when rates are down, while potential sellers have been hesitant to let go of the historically low mortgages they have on their homes. This has led to a well-known dynamic in our region: not enough inventory to meet the current demand, causing buyers to compete again in multiple offer scenarios. The likely effect of this push-pull will be higher prices in the coming months, despite the constraints of higher (and unpredictable) mortgage rates.

The current interest rate environment is the difference between the level of competition the market is experiencing now and the frenzy of the pandemic market. Buying power is lessened by higher mortgage payments, and with rates still in flux, creative financing is key for many buyers.

That being said, Windermere’s Chief Economist Matthew Gardner notes buyers are eager to take advantage of brief dips in rates when they appear. “What is interesting is that home prices rose between January and February, which tells me that buyers jumped on the opportunity to take advantage of mortgage rates that dipped below 6.1% five times between mid-January end early February,” Gardner said.

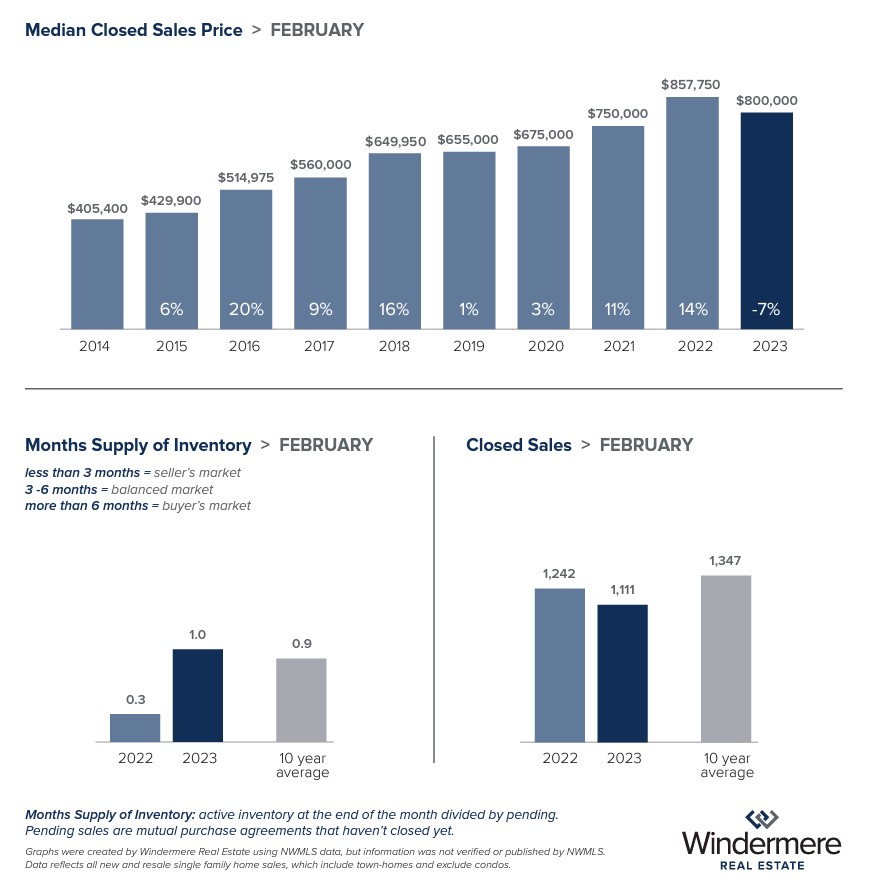

In King County, single-family home prices did rise from $781,098 in January to $800,000, though that’s down 6.7% from $857,750 in February 2022. Condos were also up, with a median price of $468,500 last month compared to $450,000 in January.

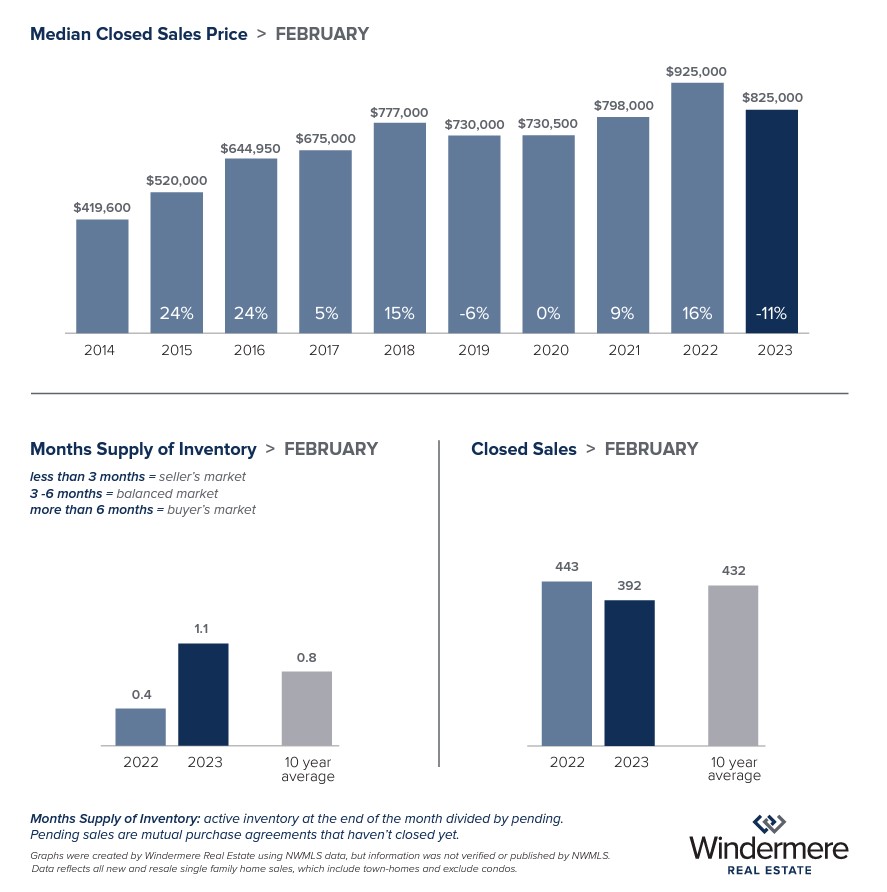

Seattle followed the same pattern, with the median price of single-family homes rising from $803,750 in January to $825,000 last month. While that is still down 11% from $925,000 this time last year, interest rates have played a large part in what buyers can reasonably afford. In the last two years alone, the median interest payment for a single-family home has risen 54%, from $3,283 in February 2021 to $5,085 — an increase of $1,802. Despite this, demand is still high, as buyers do what they can to break into the market. In February, 28% of Seattle homes sold above list price, and 53% of listings sold in under two weeks.

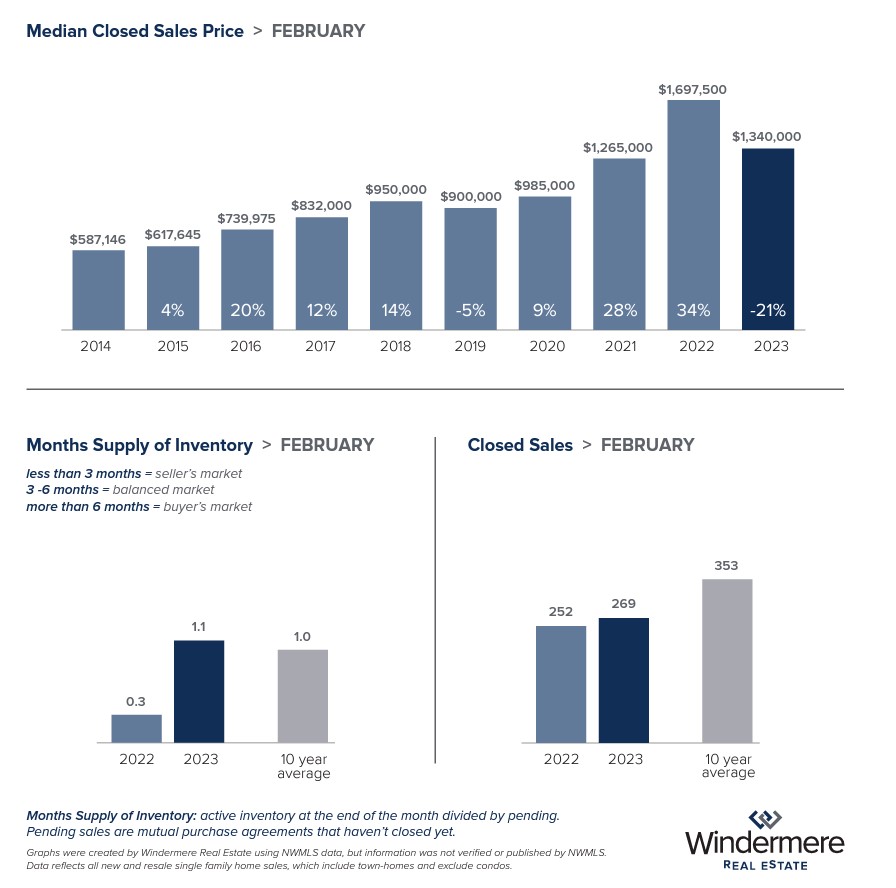

On the Eastside, the median price of a single-family home last month was $1,340,000 — down over 21% from a year ago, when the median was $1,697,500. However, February sold prices were up from January when the median was $1,320,000. A sure sign that the Eastside market is becoming more competitive, in the last three months, both the number of homes selling above the asking price and the amount over list price have doubled.

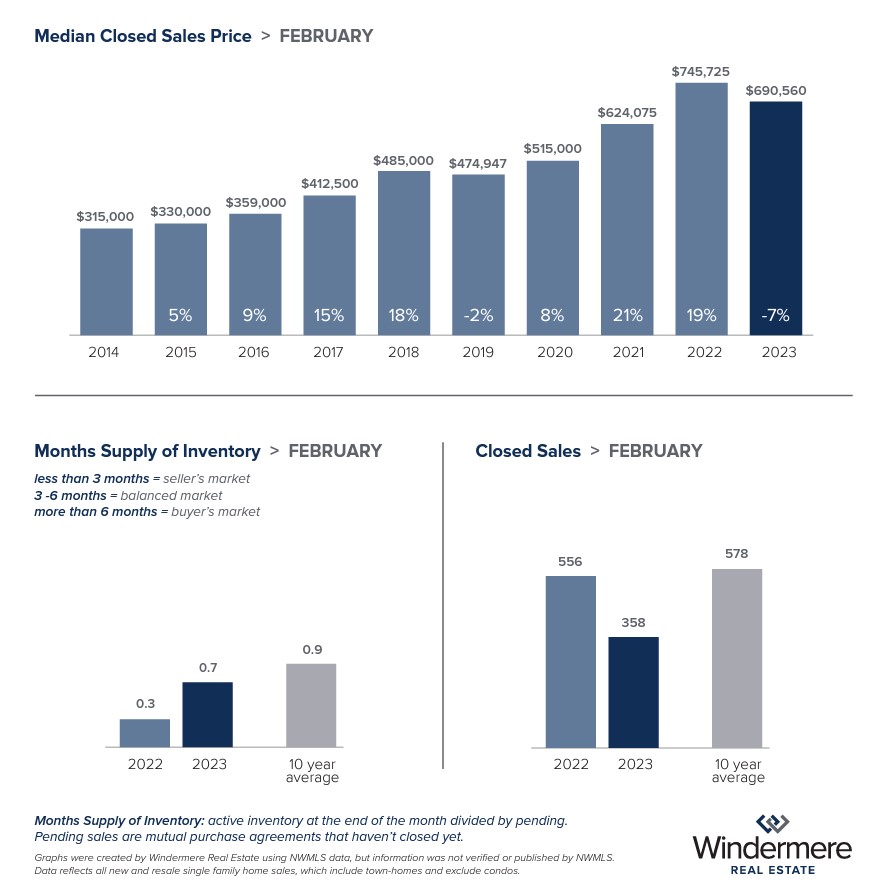

In Snohomish County, the median price for single-family homes fell 7.4% year-over-year to $690,560. Unlike the other regions, that’s also down from January’s median price of $699,000. The higher interest rates could be causing more buyers in this market to pause as they wait for prices and rates to stabilize. The relative affordability of Snohomish County has long been a draw for many buyers, who now may be more sensitive to the fluctuations of the market.

Looking ahead, Matthew Gardner predicts we will see more of the same trends. “Year over year, home sales prices are down, but that isn’t surprising given that a year ago, homebuyers were scrambling to buy in the face of mortgage rates that were about to skyrocket,” he said. “I expect we will see a similar story for the next few months.”

If you have questions about what these market conditions mean for you, please give the Kari Haas Real Estate Team a call!

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com.

January 2023 Real Estate Market Update

The close of 2022 brought the housing market extremes of the last year into sharp focus. With decreased sales, generally increasing inventory, and lower prices, the December market finally seemed to hit the winter slowdown that has characterized typical market cycles of years past. This stands in contrast to the early months of 2022, which saw sky-high prices and scarce inventory before the threat of inflation and rising mortgage rates caused the shift in the latter half of the year.

Windermere Chief Economist Matthew Gardner commented on this phenomenon. “The local housing market in 2022 ended with a whimper rather than a bang. Overall, the housing market is going to continue falling off the artificial ‘sugar high’ that was a function of the artificially low mortgage rates during the pandemic,” he said.

This is not necessarily a bad thing, as stability in the market could translate to more predictable price appreciation for sellers and better circumstances for buyers to enter the market. In most cases, it’s low- and middle-priced homes that are missing from the market, so many first-time buyers still have plenty of pent-up demand for inventory that meets their needs and financial situations.

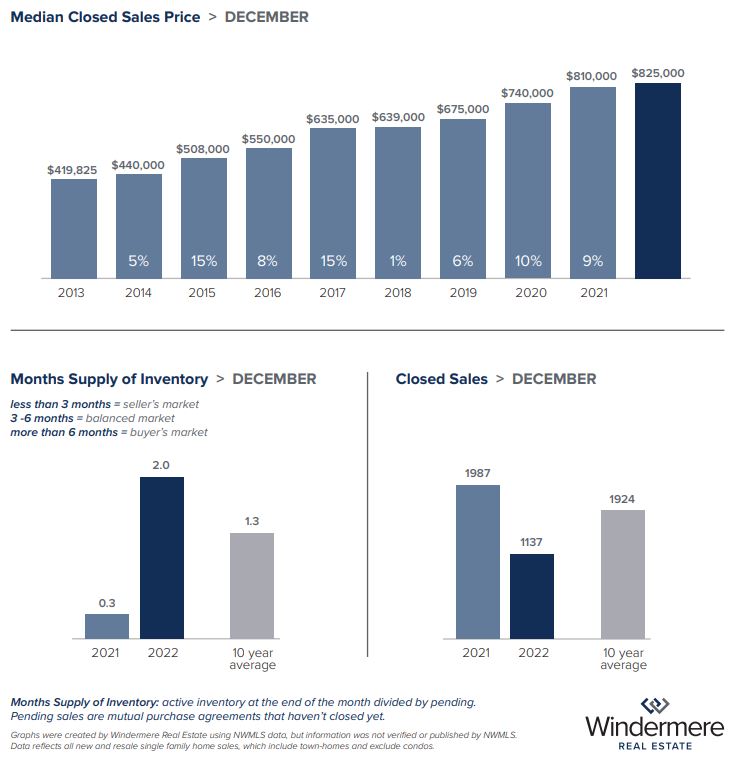

Despite a 43.3% drop in closed sales compared to December 2021, last month saw the median price for single-family homes in King County rise to $825,000. That’s up from the median of $810,000 this time last year. This could speak to the lingering effects of inflation on the market or be a factor in the lack of entry and mid-level homes currently available to buyers.

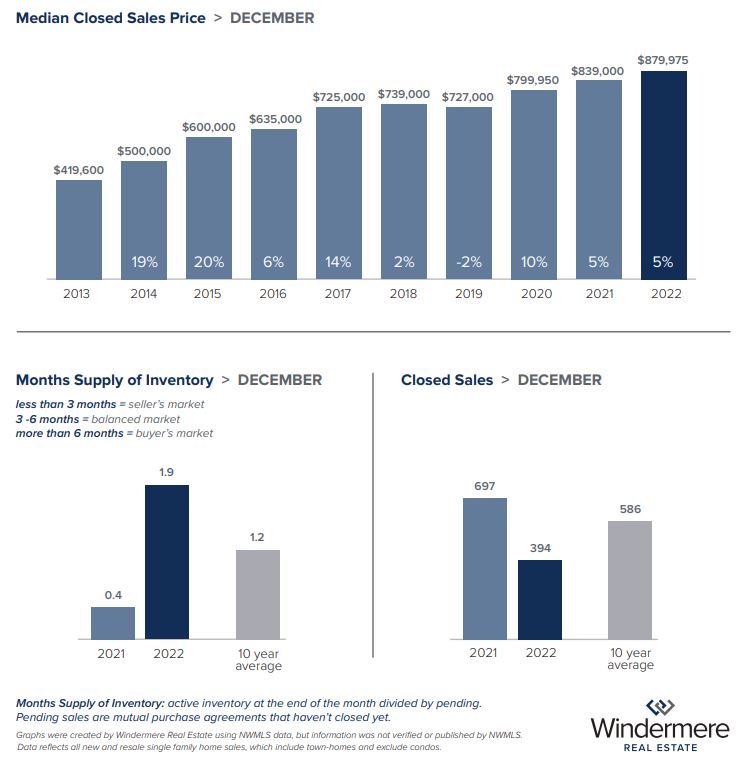

The Seattle market experienced the same pattern, with a year-over-year price increase of almost 5%, from $839,000 in December 2021 to $879,975 last month. Closed sales were down in the city as well, dropping 43.5% from last year to just 394 units, leaving the market with just under six weeks of inventory. The condo market mimicked this trend, with the median price rising to $512,500 last month, up from $490,000 in December 2021. Additionally, Seattle condos offered the highest amount of inventory, with 2.5 months of stock.

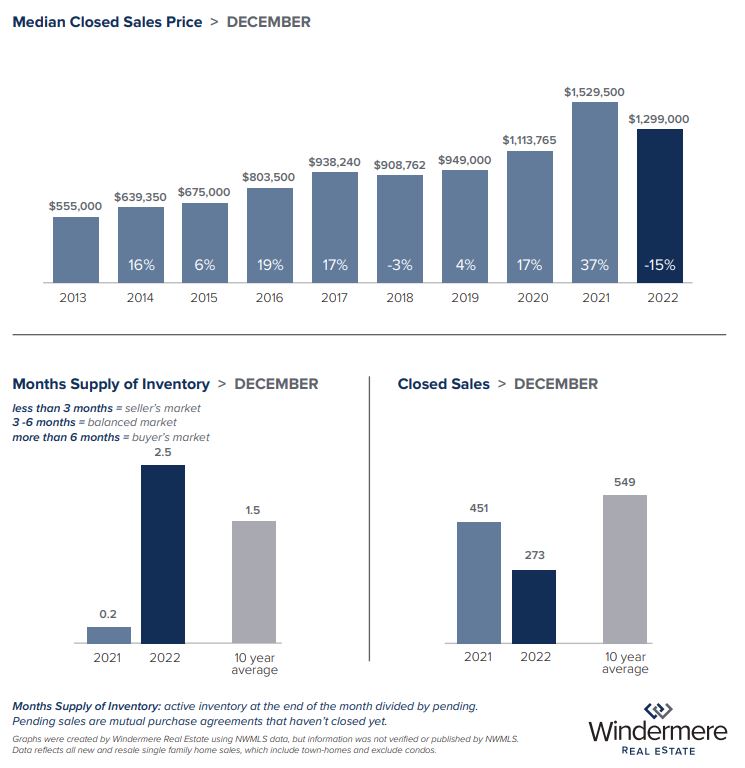

Things were a little different on the Eastside, which had experienced perhaps the highest price boom during the “sugar high” of the pandemic. There, single-family home prices decreased around 15% year-over-year, landing at a median of $1,299,000 last month, compared to $1,529,500 in December 2021. This is likely due to higher mortgage rates dampening the buying power of potential homebuyers in the area. Entry-level buyers may be forced to look in more affordable markets for the time being, and December’s 39.5% decrease in closed sales compared to December 2021 reflects this. Interestingly, Eastside condos experienced a sold price increase to a median of $565,000, up from $550,000 last year. This is likely because condos are a much more affordable entry point to the Eastside market and may be experiencing higher demand as buyers tailor their expectations to the current market conditions.

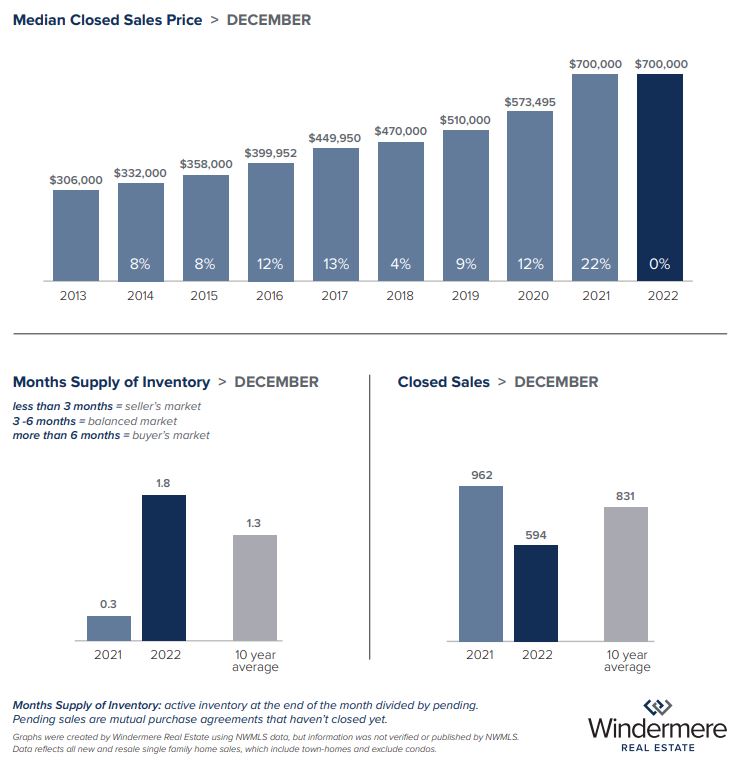

After the ups and downs of the last year, Snohomish County ended exactly where it began, with a median single-family home price of $700,000 — the same as in December 2021. Closed sales in the area were down 38.3%, leaving the market with about six weeks of inventory. Throughout the pandemic, Snohomish County has been a relatively stable market compared to the fluctuations of Seattle and the Eastside, making it a desirable area for first-time buyers and those looking to maximize their buying power.

Looking ahead, Matthew Gardner expects 2023 will see continued price declines. However, “With mortgage rates expected to fall from current levels slowly, sale prices should start increasing again in the second half of the year,” he said.

Gardner continued, “Ultimately, once prices pull back to where they would have been if the pandemic had never occurred, they will start to stabilize and then return to a more normalized pace of appreciation.”

Sellers and buyers have certainly felt the impacts of shifting economic conditions on the housing market. A slower market pace and modest price decreases may be necessary to help reset expectations on both sides and set up sustained future success.

If you have questions about how to make the most of the current market conditions, give Kari a call.

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com.

November 2022 Real Estate Market Update

As the final quarter of 2022 rolls on, it’s clear that these last months will be anything but typical for home buyers and sellers in King and Snohomish counties. In a real estate market that’s been defined by high competition and low supply for the last number of years, buyers and sellers are changing tactics as market dynamics shift due to rising mortgage rates and growing inventory.

While some buyers are waiting to see if rates and home prices drop, others are getting creative with their financing by utilizing buydowns, adjustable rate loans, carrying back second deeds of trust, and closing cost allowances to make their purchases. Sellers have been slower to adjust, with many resisting the idea of lowering their asking price to meet the constraints of buyers dealing with high-interest rates. However, for sellers willing to correctly market and position their listing, successful sales – and even occasionally multiple offers – can still be attained.

Seattle & King County

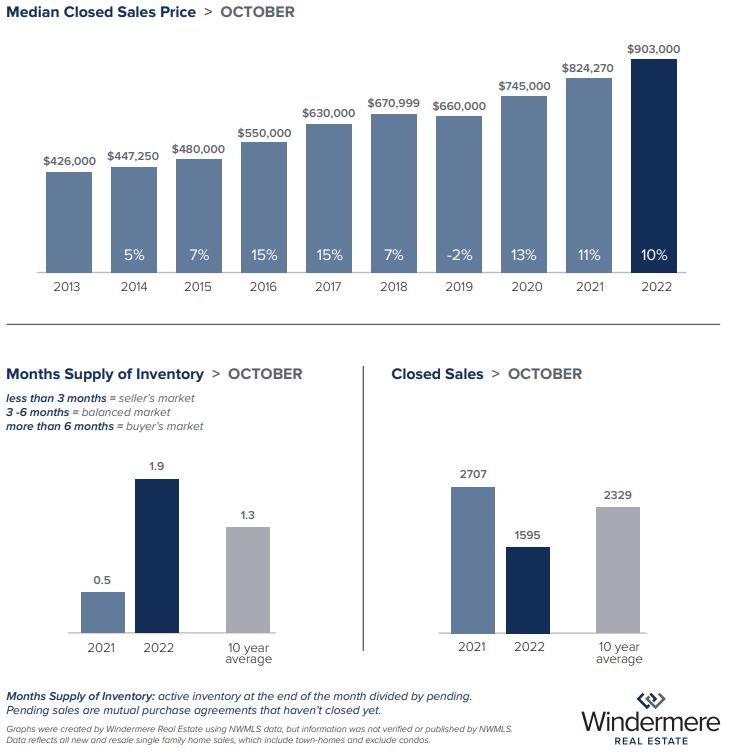

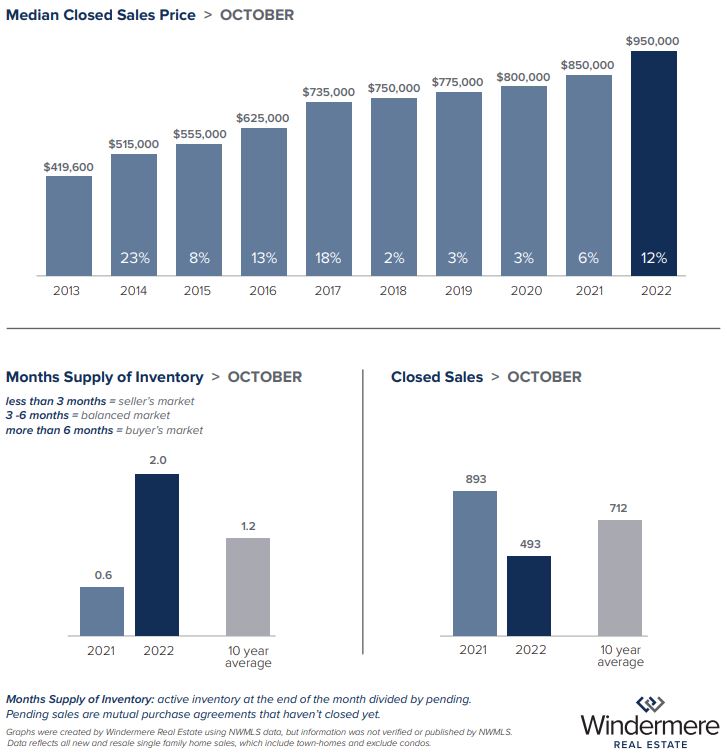

King County as a whole saw the median price of a single-family home increase from $875,000 in September to $903,000 last month. This was primarily a function of price gains in Seattle, where single-family homes sold for a median of $950,000 in October — up from $900,000 in September. Seattle and King County both have about two months of available supply, which is the most balanced inventory level the market has seen in years. The Seattle condo market has slowed a bit more than residential sales, with over 3 months of inventory and a median price of $522,500 — down from $525,000 year-over-year.

Eastside

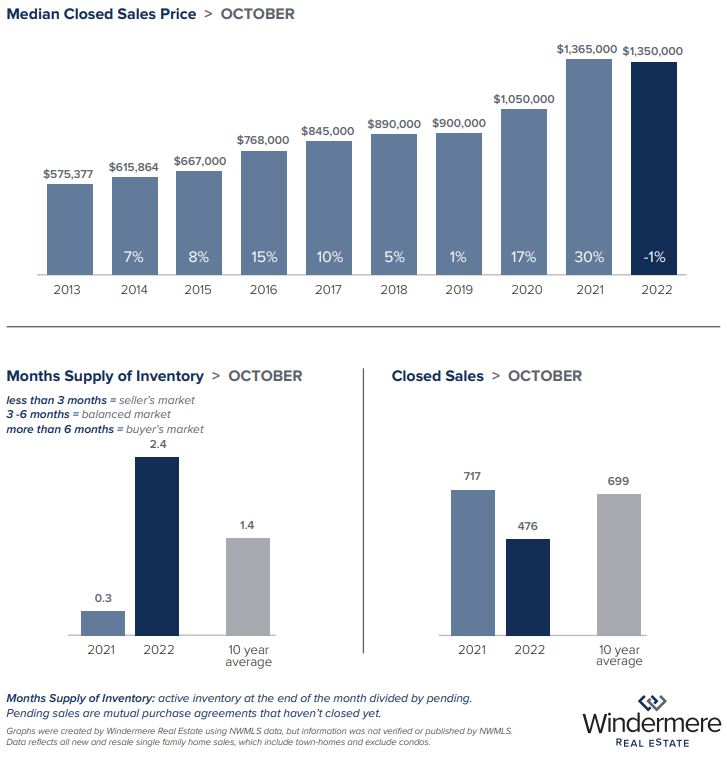

On the Eastside, the median price for single-family homes has remained constant, sitting at $1,350,000 for the third month in a row. The average monthly mortgage payment on the Eastside dropped 19% from $9,226 in April 2022 (when the median price was $1,722,500 with a 4.98% interest rate) to $7,430 in August 2022 (with a median price of $1,350,000 at a 5.22% interest rate). However, while the median price has remained the same since August, the 30-year interest rate rose to 6.9% in October. At that rate, the average monthly payment is $8,891 — only 4% off the peak payment of $9,226 in April; this is despite a 22% drop in prices since then.

Snohomish County

Snohomish County saw prices fall slightly from a median of $735,000 for single-family homes in September to $730,000 last month. With less than two months of inventory, that market remains slightly more competitive than the Eastside or Seattle, possibly due to lower prices making it more accessible for buyers as they combat the higher interest rates.

Matthew Gardner’s Take

Windermere’s Chief Economist Matthew Gardner weighed in on the effect of mortgage rates on buyer behavior. While he believes many buyers may be forced to wait (either voluntarily or not) for interest rates to stabilize, he advises would-be buyers not to wait for prices to bottom out. “Those who hope to pick up a home ‘on the cheap’ are likely in for a long wait,” he said.

For many buyers, the answer to this conundrum is a pivot to adjustable rate mortgages, which are currently set at around 5.9%. With the 30-year fixed mortgage rate currently at 6.9% or higher, adjustable rate mortgages offer a more affordable inroad to homeownership, with the possibility of refinancing to a lower rate in a few years.

As we navigate these changing market conditions, Kari can help you assess the best path forward for your home sale or purchase.

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com.

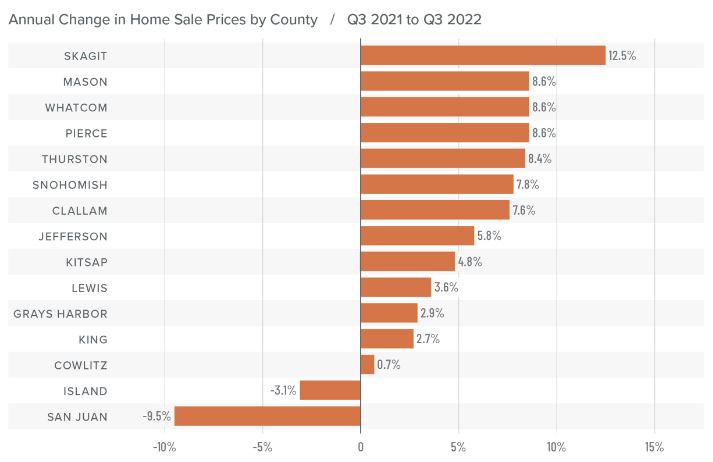

Q3 Western WA 2022 Gardner Report

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact Kari.

REGIONAL ECONOMIC OVERVIEW

The Western Washington labor market continues to expand. The addition of 110,000 jobs over the past 12 months represents an impressive increase of 4.9%. All but seven counties have recovered completely from their pandemic job losses. In total, the region has recovered all the jobs lost and has added an additional 30,000 new positions. The regional unemployment rate in August was 3.8%. This is .2% higher than at the end of the second quarter. That said, county data is not seasonally adjusted, which is likely the reason for the modest increase. The labor force has not expanded at its normal pace, which is starting to impact job growth. Although the likelihood of a recession starting this winter has risen, Matthew Gardner is not overly concerned; however, he anticipates businesses may start to taper hiring if they feel the demand for their goods and services is softening.

WESTERN WASHINGTON HOME SALES

❱ In the third quarter, 19,455 homes traded hands, representing a drop of 29.2% from the same period a year ago. Sales were 15.4% lower than in the second quarter of this year.

❱ Listing activity continues to increase, with the average number of homes for sale up 103% from a year ago and 61% higher than in the second quarter of 2022.

❱ Year over year, sales fell across the board, but when compared to the second quarter they were higher in Mason, Cowlitz, Jefferson, and Clallam counties.

❱ Pending sales (demand) outpaced listings (supply) by a factor of 1:6. This ratio has been dropping for the past three quarters and indicates a market moving back toward balance. The only question is whether it will overshoot and turn into a buyer’s market.

WESTERN WASHINGTON HOME PRICES

❱ Higher financing costs and more choices in the market continue to impact home prices. Although prices rose an average of 3.6% compared to a year ago, they were down 9.9% from the prior quarter. The current average sale price of a home in Western Washington is $748,569.

❱ The change in list prices is a good leading indicator and we have seen a change in the market. All but two counties (Island and Jefferson) saw median list prices either static or lower than in the second quarter of 2022.

❱ Prices rose in all but two counties, and several counties saw price growth well above their long-term averages.

❱ With the number of homes for sale rising and list prices starting to pull back, it’s not surprising to see price growth falter. We are going through a reversion following the overstimulated market of 2020 and 2021. There will be some ugly numbers in terms of sales and prices as we move through this period of adjustment, but the pain will be temporary.

MORTGAGE RATES

❱ This remains an uncertain period for mortgage rates. When the Federal Reserve slowed bond purchases in 2013, investors were accused of having a “taper tantrum,” and we are seeing a similar reaction today. The Fed appears to be content to watch the housing market endure a period of pain as they throw all their tools at reducing inflation.

❱ As a result, mortgage rates are out of sync with treasury yields, which not only continues to push rates much higher but also creates violent swings in both directions. My current forecast calls for rates to peak in the fourth quarter of this year before starting to pull back slowly. That said, they will remain in the 6% range until the end of 2023.

DAYS ON MARKET

❱ It took an average of 24 days for a home to sell in the third quarter of the year. This was seven more days than in the same quarter of 2021, and eight days more than in the second quarter.

❱ King and Kitsap counties were the tightest markets in Western Washington, with homes taking an average of 19 days to sell.

❱ Only one county (San Juan) saw the average time on the market drop from the same period a year ago. San Juan was also the only county to see market time drop between the second and third quarters of this year.

❱ The greatest increase in market time compared to a year ago was in Grays Harbor, where it took an average of 13 more days for homes to sell. Compared to the second quarter of 2022, Thurston County saw the average market time rise the most (from 9 to 20 days).

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Listings are up, sales are down, and a shift toward buyers has started. After a decade of sellers dominating the market, it is far too early to say that the shift is enough to turn the market in favor of buyers, but the pendulum has started to swing in their direction.

A belief that the housing market is on its way to collapsing will keep some buyers sidelined, while others may be waiting for mortgage rates to settle down. Whatever their reasons, Matthew Gardner maintains that we will see a brief period where annual price growth will turn negative in several markets, but it is only because the market is normalizing. He certainly doesn’t see any systemic risk of home values falling as they did in the mid-to-late 2000s.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

This post originally appeared on the Windermere.com Blog.

How to Make Moving to a New State Hassle-Free

Moving to a new state is a big adjustment and can be draining. However, having the right information can make it less challenging. Here are some tips from Kari Haas Real Estate Team on how to make moving to a new state hassle-free and help you make the transition as smooth as possible.

Find a Job

If you’re moving to a new state, you’ll need to find a job in your new location. Check out job boards or networking in your new city to find job openings. Your job search should start with finding who needs your skills in the new state. Also, update your resume and cover letter to match the new job market. And if you’re moving to a new state, make sure you find information about the cost of living, as well.

Start a Business

Starting a new business in a new location can be daunting. Here are the steps to follow:

- Get familiar with laws and regulations. Research the laws and regulations regarding starting a business in a specific state.

- Choose a business location. Pick a convenient location that suits your budget and needs.

- Craft a business plan. Create a detailed outline of the services or products you’ll be selling, how to structure the business, your financial projections, and funding options for your new business.

- Create a plan of action. Craft a plan of action to follow since starting a business can be chaotic. If possible, create a team and delegate tasks.

Also, don’t forget about marketing! A lot of your advertising can be done through social media platforms, which will save you lots of money. However, you should also spend some time on content marketing, which means generating interest in a topic rather than simply advertising a specific product. This is a great way to build your customer base from the ground up, and Cornerstone Content can help you get started.

Adjust to the New Location

When you first move to a new state, it can be difficult to figure out where everything is. Take the time to familiarize yourself with your new surroundings. Explore your new city and find things to do that you enjoy. Consider joining social groups in your new state and making friends. You’ll also need to adjust to the weather in the new location.

Ready To Move?

Moving can be challenging but it’s also an exciting opportunity to start a bold new chapter of your life. Also, you can greatly reduce stress by doing some simple research and preparation beforehand. Research the job market, familiarize yourself with your new setting, and you’ll feel right at home in no time!

Kari Haas Real Estate Team exudes a passion for real estate that carries through to every client. Call 206-719-2224

Image via Pexels.

This post was originally written by Lisa Walker and was submitted exclusively to KariHaas.com

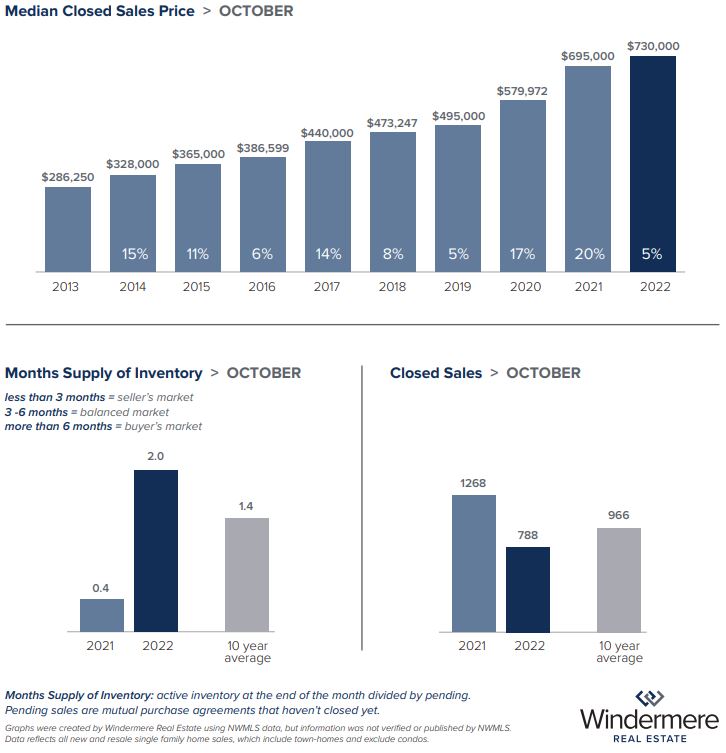

October 2022 Real Estate Market Update

Increasing listings inventory, lengthening time on the market and a slowdown in home price increases across the Puget Sound region herald a return to normalcy and better opportunities for buyers. According to September data from the NWMLS, active listings nearly doubled from a year ago, with pending sales declining by about 31%.

“The ‘Great Reversion’ continues, with the number of homes in the tri-county market of King, Pierce, and Snohomish counties up 106% from a year ago,” says Windermere’s Chief Economist Matthew Gardner. “It’s worth noting that current inventory levels in King and Snohomish counties are still around 13% lower than they were in September 2019 prior to the pandemic-induced market shift.”

While the recent sales data may be pointing to a market shift of a different sort, they may reflect some normal seasonal trends as well. October is typically an average selling month, with November typically performing about 76% as well as an average month, and December and January slowing even further as the holidays and end of year pull some buyers from their home searches.

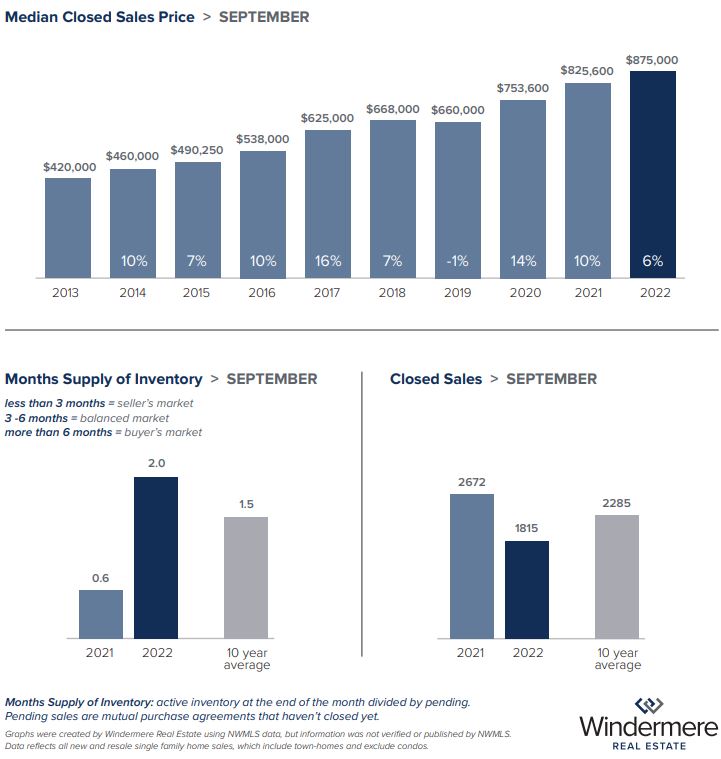

That being said, last month still saw year-over-year price increases in Puget Sound’s busiest metros, despite some month-over-month price dips. King County single-family homes saw a price decrease from $899,999 in August to $875,000 last month. That’s still up from last September’s median price of $825,600, and condos also saw year-over-year price increases, from $466,501 last September to $483,000 this September. With about two months’ inventory for both housing types, King County buyers are better able to take their time and consider the details of their purchase.

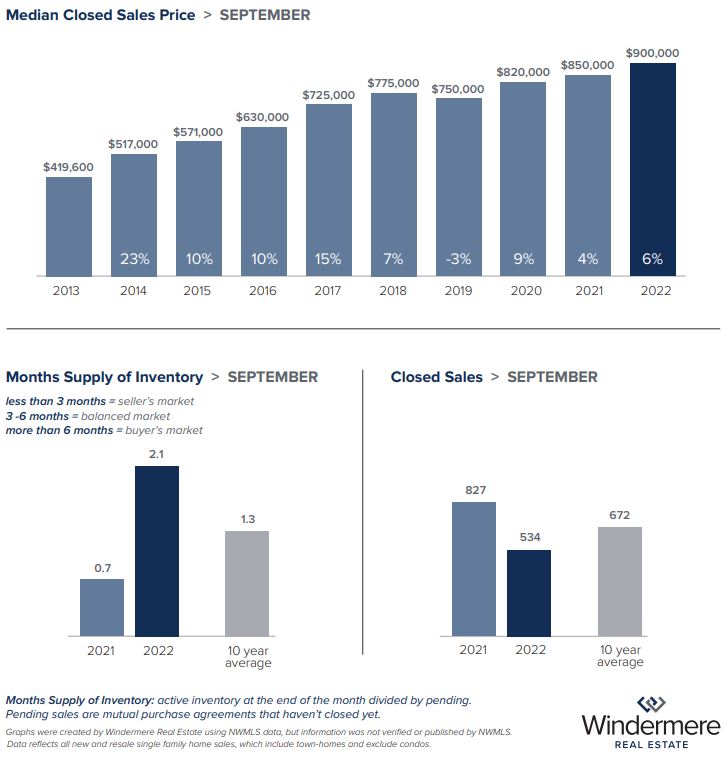

Seattle also saw a slight month-over-month decrease in single-family home prices, from a median price of $927,000 in August to $900,000 last month. That’s still up six percent from $850,000 in September 2021. Conversely, year-over-year condo prices slumped a bit, falling to $499,000 last month from $505,000 in September 2021. Condo inventory has also increased, with buyers benefitting from over two months’ supply. Sellers are encouraged to price wisely and accurately to beat the competition in these conditions.

The Eastside was the only area to see prices stay the same month-over-month, with the median price for a single-family home remaining constant at $1,350,000. That’s an increase from the median price of $1,310,000 in 2021. Active inventory also increased, up to 1.9 months’ supply. The last time the Eastside had this many listings (approximately 1,200) was before the pandemic in 2019.

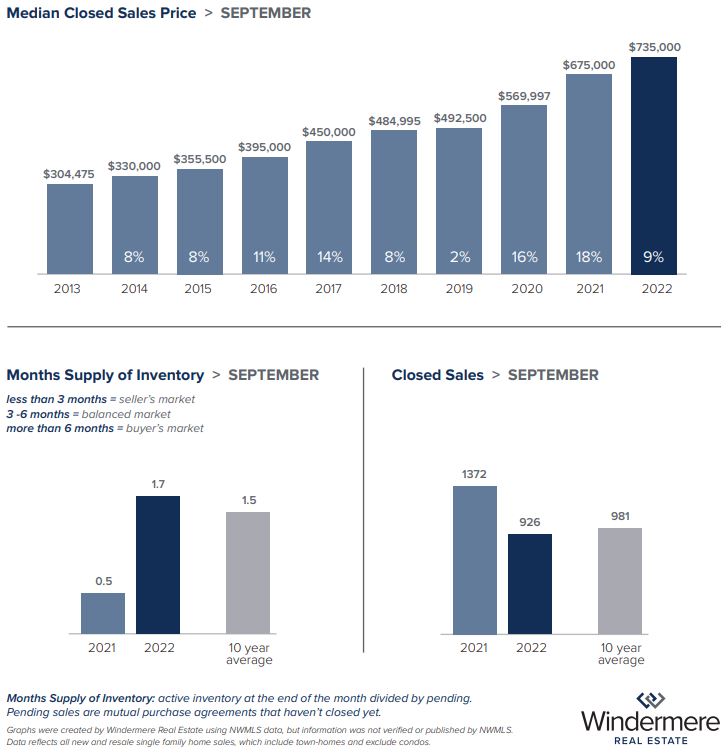

Snohomish County followed Seattle and King County, with prices dropping slightly to a median of $735,000 for single-family homes last month — down from $749,000 in August. Inventory was slightly tighter in the area, with about 1.75 months’ supply, though it’s still an improvement over the tight inventory at the height of the pandemic.

Many buyers are feeling a bit of a “pandemic hangover” when it comes to interest rates, which may be contributing to the increase in inventory across the region. The conditions that led to the historic low-interest rates were unprecedented, and buyers now need to be willing to consider buying at a higher rate with the goal of refinancing later on if they’re able.

The future of the local market will be dictated by fluctuations in interest rates. If rates increase from the September average of 6.11%, real estate experts expect new pending sales to continue to be 25% – 30% below the prior year in units. Median closed sale prices will roughly decline 10% for each 1% increase in interest rates. However, if interest rates decline from the September average, we can expect pending sales to increase, prices to remain flat, and active inventory to decline more than normal.

Matthew Gardner also points out that home prices “remain positive compared to a year ago.” He doesn’t expect this to change by the end of 2022. By spring, however, Gardner believes “it’s likely that year-over-year prices will start to trend negative. That said, I firmly believe that this will only be a short period of correction, so homeowners in the Puget Sound area shouldn’t be too concerned, especially given that 64% of them are sitting on over 50% of home equity.”

If you have questions about how home inventory or inflation could impact your position in the real estate market, please call the Kari Haas Real Estate Team.

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com.

What to Ask Your Financial Planner Before Buying a Home

US home prices continue to rise in 2022. Just last March, prices spiked at a rate of 20.6%, making it the highest year-over-year price change in over 35 years. With rapid home price surges across 20 different US cities, it’s crucial for aspiring homeowners to consult with financial planners to better navigate the pressures of enlarged home values. That being said, demand for personal financial advisors has likewise increased; their employment rate is even set to grow by 15% in the following years. As formal finance education now focuses on investment strategies and securities analysis, planners can make informed recommendations according to your income, debt, and credit history. This advice will help you manage the potential risks and returns when purchasing a house. For instance, finding the right mortgage can help homebuyers retain a decent part of their gross income, and meet future maintenance and repair costs better.

The questions you ask your financial planner before purchasing a house can lead to a more well-rounded decision. We’ve listed below the four questions you need to start with.

1. How much can I actually afford?

Mortgages are quite costly and can affect your plans of buying your dream home. As it stands, a $300,000 loan, for example, can require you to pay $1,734 a month. Now although financial calculators prove beneficial in planning your budget, they aren’t enough. It’s important to seek advice from a financial planner on how much you should save for house costs. Consulting a professional is especially relevant if your budget oversees non-negotiable costs like student loan debt. Financial planners can identify your debt to income ratio, which is used when you apply for a mortgage, and suggest how much you should borrow — this way you don’t have to stretch your budget thin.

2. What type of mortgages can I pick from?

Your financial planner can present a selection of mortgages that are proportional to your financial situation. Below are some of the mortgages you can apply for:

Conventional loans

These loans require a strong credit score and come in two types: conforming and non-conforming. Conforming loans, specifically, follow a set of standards for loan size, debt and credit created by the Federal Housing Finance Agency. Most areas have a loan limit of $647,200, while expensive locations go up to $970,800, so it’s best to talk to your planner to know how much you can take out for your home — especially if you want to purchase a house in expensive areas.

Government-backed loans

FHA, USDA, and VA are among a few examples of this loan. There are varying conditions for each, like how much money should be put down, and your planner can see if you qualify for these loans. Typically, VA or USDA loans need high credit scores, whereas FHA loans require much steeper down payments. Also, if you aren’t within a low-to-moderate income level or don’t prefer a home in rural areas, your advisor might warn against taking out a USDA mortgage.

3. How much do home insurance policies go for?

Alongside your mortgage plan, financial planners make sure you get the right insurance coverage for your needs. Insurance plans should correspond to the type of coverage your house requires, and planners can base them on the home’s past claim history and physical condition, as well as its location. On average, the cost of homeowners insurance policies in the US amount to $1,312 annually for a $250,000 dwelling coverage amount. If you live in disaster-prone areas, however, insurance premiums can rise up to 12.1%. Ultimately, home insurance policies differ across different houses, so speak to your planner about which coverage best suits you.

4. Should I place my home in a trust?

Houses are large purchases that double as assets. Consult your financial planner about having your home protected through an estate plan (which transfers any legal responsibility of your assets to trusted loved ones). In particular, trusts enable you to pass down your home to another. Depending on your home’s value, planners can recommend whether a trust is beneficial for you. A house worth $160,000, for instance, can be included in a trust. Trusts are ideal if you’re buying an expensive home, as they prevent your family from undergoing probate court to contest homeownership rights. If you’re worried that placing your home under a trust means losing control over the property, don’t be. As your financial planner will affirm, a trustee can choose how and when their beneficiary will inherit the house.

Finding your Financial Advisor with Kari Haas

The Kari Haas Real Estate Team works closely with a trusted Financial Advisor and has connections and referrals for you in all steps of the home buying/selling process. Give Kari a call to be connected with one of our highly recommended service providers.

Article exclusively submitted to karihaas.com

Written by Rita Janine

Image via Pexels

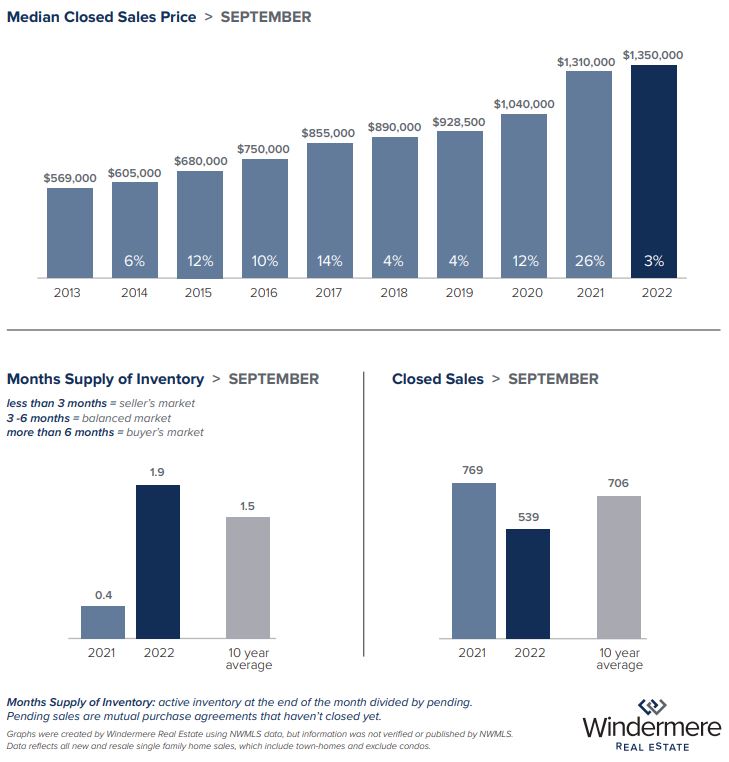

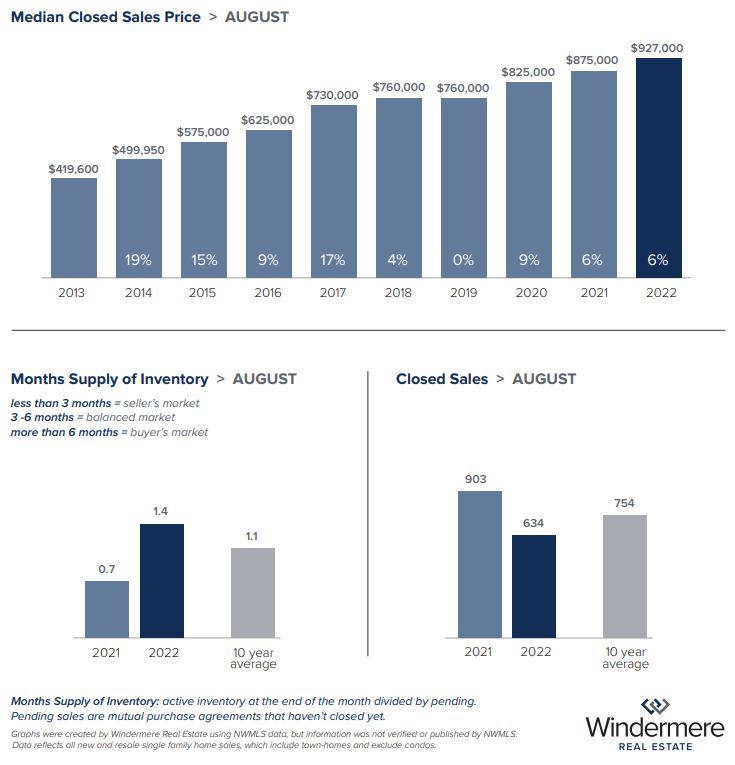

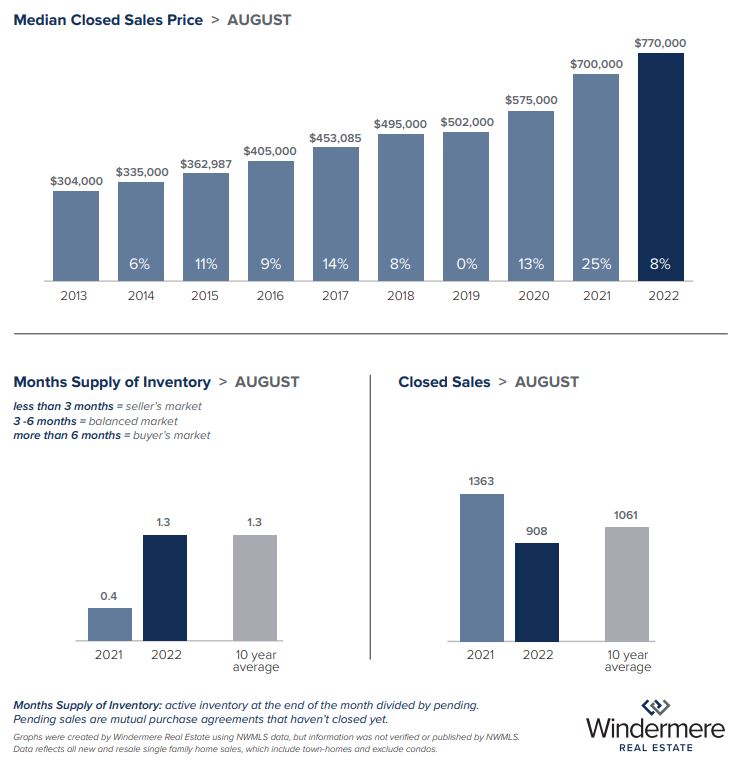

September 2022 Real Estate Market Update

After its breakneck pace over the last two years, it appears the housing market has finally reached a soft bottom to the price corrections that began in April of this year. Reports that we’re entering a bear market are generally exaggerated, however, as the market seems simply to be resetting to a more balanced state where buyers and sellers are at last on more equal footing. Perhaps as much as anything, the market’s performance in August reflects a typical pattern for a month that has traditionally been a slower time for housing sales.

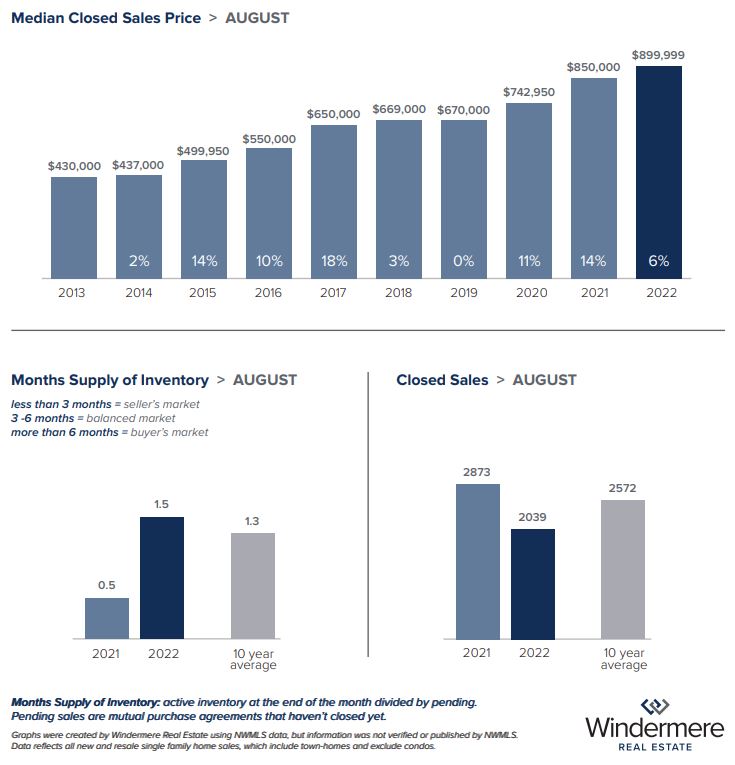

In King County last month, available inventory declined slightly to 1.5 months’ supply, with the median home price of $899,999 up slightly over July’s median of $890,000. That’s also an increase of 5.8% from $850,000 in August 2021. With 57% of homes selling in under two weeks and 22% selling over list price, many King County home buyers still have to move quickly and competitively, although with more leverage than they had earlier this year thanks to recent supply increases.

The Eastside had slightly higher levels of housing inventory available, at about 1.6 months. The median sold price for single-family homes rose 4% year-over-year, to $1,350,000. The higher asking prices in this area mean fewer homes are selling over asking than in Seattle, with about one in four homes selling at or over list price. Condos remain a more affordable option in this highly desired area, with the median price for an Eastside condo sitting at $569,500 last month.

Seattle has slightly less supply than King County as a whole, sitting around 1.4 months of inventory. The median sold price for single-family homes was up 6% year-over-year, at $927,000. About 65% of single-family homes in the city sold within two weeks, while 26% of homes sold above list price. With 2.4 months of inventory, condos may offer buyers an easier way to break into the market. The median sold price for condos last month was also a more affordable $520,000, though that’s still up 8.3% year-over-year. Increasing rents in the city and across the Puget Sound region are driving some buyers into the market, as homeownership is a hedge against inflation and rising rent costs. Even with that in mind, sellers still need to price accurately to avoid their homes sitting on the market for too long.

Snohomish County had the lowest inventory level at 1.3 months of supply (which is still more than the county’s average the past few years). The median sold price for single-family homes was $749,999, which is up 8% from August 2021. Just over half of the available homes sold within two weeks, and 19% sold over list price. The median price for condos in Snohomish County fell almost 5% year-over-year, landing at $474,999. This area continues to be a draw for buyers who may be priced out of the Seattle and Eastside markets.

Windermere’s Chief Economist Matthew Gardner believes the decrease in prices is a sign we’re entering a more typical housing market than we’ve seen in the last few years. “Home sales increased month-over-month, but the rise in listings is causing prices to soften,” he said. “I predict prices will drop further as we move into the fall. The market is simply reverting to its long-term average as it moves away from the artificial conditions caused by the pandemic.”

EASTSIDE

KING COUNTY

SEATTLE

SNOHOMISH COUNTY

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com

Upsizing for Retiring: Find a Home for Your Homestead

Some retirees plan to downsize their lives and homes after a while, ostensibly to make things simpler and to have less baggage in retirement. But you’re different: You want to upsize and pursue a grander new life of homesteading as a retiree, with enough space to welcome family whenever they wish to visit, pursue crafts you never got to do, and create a different kind of life that you never got to experience.

The good news is that it is within your power to create the homesteading life you wish to live. Here are some tips from Kari Haas for finding a new home that will help you build the kind of self-sufficient environment you seek:

Look for the right kind of home

For true self-sufficiency and proper homesteading, Treehugger notes that you’ll need a large space—in both land and square footage of your house. Before you get a loan or do any specific research, know your budget and make a list of features that you will prioritize. Do you want a large enough plot of land so that you can raise horses? The Extension Foundation notes that one to two acres is a general rule of thumb when it comes to land needed for a horse to forage (30-38 acres per horse for non-irrigated dryland pastures).

Do you want enough room for a workshop—enough land to build one after the fact or one already on the property? Do you want to have enough space to have a large garden? Write these down to identify which are most important to you.

Hire a realtor

This could be the most crucial step in the process of buying your new home. They are practically necessary if you’re both buying and selling a home simultaneously. Having someone like Kari Haas on your team who understands the market, knows what you’re looking for, and can negotiate on your behalf is an incredible advantage. Realtors pay attention to details that you may not even think of, as well. If you have a real estate agent sell your current home, there’s a better chance of it selling at a higher price—there’s data to back it up.

Make sure you can afford your new home

A huge part of upsizing is making sure you have enough funds to afford the bigger space. You may be able to sell your old house and, thereby, cover the majority of the cost of moving into your new homestead. Just make sure you research the number of properties available in your area and check the property prices in your area and get a handle on how much similar houses are selling for, especially as the market fluctuates.

Start a new business in your home

As a retiree, you have time now to pursue activities you didn’t necessarily have the bandwidth for when you were working full-time. Why not turn those hobbies into a business to make money on the side? Not only will it help you afford your new home, but it will present you with an opportunity to do something fulfilling and provide a service or products to other people.

If you do decide to start a small business, consider using a formation service to form a limited liability company (LLC) to limit your liability, get personal asset protection, and enjoy tax advantages. Make sure to check on the rules of forming an LLC in the state so you’re up to speed.

There are countless options out there for aspiring and ambitious entrepreneurs – not to mention ways to streamline your business for the new age! For instance, if you’re looking to automate your business, spend some time getting acquainted with the leading robotics companies that are helping to shape the future of technology.

With a good amount of research and due diligence, finding a home for your homestead is certainly within reach. Follow these guidelines and you’ll be up and running in no time!

Whatever your real estate needs, Kari Haas can help you reach your goals with confidence.

Call 206-719-2224

Image via Pexels

This post was originally written by a guest blogger, Ray Flynn

6 Tips for Moving and Starting Over in New State

Moving is both exciting and overwhelming at the same time. Without proper planning, it can become chaos, slowing down your chance to adjust quickly to your new home. If you’re moving to a new state, you may come across even more obstacles. Consider these tips to help you simplify the process.

-

Start Planning Far in Advance

Planning a move properly means starting the process far in advance. For example, research shows that you should have enough to cover at least three months of expenses before you move. Start the packing process at least two months before the moving date, and consider putting items in storage if you’re not sure you want to take them or think you may not have room. You can find storage companies that offer discounts, such as a month free, for new customers.

-

Consider Location When Looking for a Home

Talk to a local real estate agent before you start looking for a home in your new state. Kari Haas can help you find your dream home. Your goal should always be to find a place that best suits your needs in a location you love. Remember, location is often the most important aspect when searching for a home. You want an agent who can tell you about the school districts and shopping available in the area. A more desired location will cost more, but it will also have a higher resale value.

-

Starting Your Own Business

If you’re thinking about starting your own business in your new location, make sure you have all the plans in order before you make the big move. Create a thorough business plan to help you stay on track and show potential investors what your company has to offer. Your plan should include an executive summary about the business and products or services you’ll provide, how you plan to structure your business, any funding you will need, and any financial projections you’ve made about the company.

-

Join Your Community

If you’re looking for ways to get involved in your new community, join local social media groups or look for a community app where you can access local news and necessary information. Introduce yourself to neighbors virtually and in person to get to know people quickly. Being more involved helps you adjust more quickly.

-

Consider Investing in a Home Warranty

A home warranty is a service contract that covers the repair or replacement of major home appliances and systems, such as air conditioning, electrical, plumbing, and more. Many homeowners choose to get a home warranty to protect themselves from the high cost of repairs and replacements. Home warranties typically cover items for one year and can be renewed annually. When you’re weighing home warranty cost vs benefit, be sure to look over the home inspection report to see if there are any red flags.

-

Figure Out Your New Cost of Living

One of the first things you should do is research the cost of living in your new state. Start by looking for averages of things such as rent or mortgage, food, education, and entertainment. In Washington, housing costs are above the national average, but you can expect to pay less for health care and utilities. Washington is home to some of the best public schools in the country, so you can find affordable education for your children.

Before moving to a new state, choose a location, learn about the cost of living, consider investing in a home warranty, and think about starting a new business. Once you’ve completed your move, you’ll be ready to settle into your new life. Take the time to get to know your area, and you’ll speed up the process of feeling comfortable. Focusing on the positives of the move will help you overcome any possible homesickness.

Image via Pexels

This post was originally written by a guest blogger, Lisa Walker.